THE C-SUITE IS HELL-BENT ON TACKLING BUSINESS TRANSFORMATION AND ONE OF THE KEY AREAS OF FOCUS IS THE EFFECTIVE USE OF DATA AND ANALYTICS.

THE ELEPHANT

Every boardroom has an elephant … or two. These elephants are the looming issues everyone would rather discuss another time. The questions yet to be asked — by a person willing to ask them. It’s a common phenomenon that in today’s complex business environments, executives put off focusing on vital business issues that are not openly discussed in terms of their urgency and impact. Want to know where the elephant is when it comes to balancing the future with the present? Look at your progress on the big bets driving that future.

Balancing investment for the future with the needs of sustaining success in your current business model can often seem like a mutually exclusive proposition – particularly when the transformations required to deploy future-enabling capabilities, technologies and systems can be so disruptive to the conduct of everyday business. With the complexities of today’s marketplace, industrial companies are constantly grappling with how to pace investments and actions to best align with customers and partners in a way that optimizes value in both the short and long term.

Engaging with the challenge doesn’t diminish the size of this elephant: How does one plan for future economic viability while sustaining current economic viability?

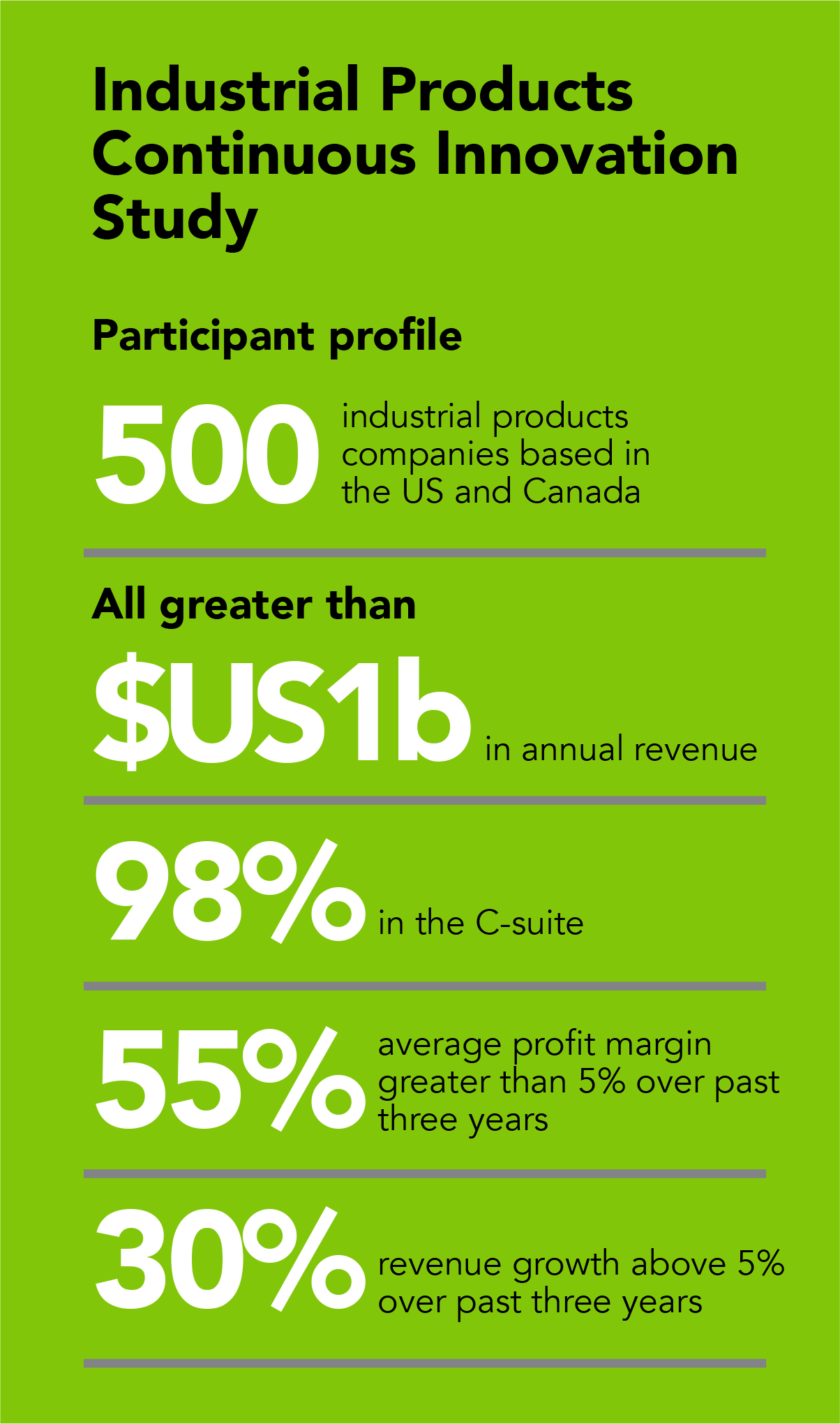

It is a dilemma so trenchant that EY recently conducted a major study to see how industrial companies were cracking the code of this balancing act. After surveying 500 senior industrial-company executives, nearly all C-suite officers from 500 discrete companies, we found that while some companies were making progress, only a handful of our respondents represented companies that were showing the results and characteristics we would associate with leadership in managing the balancing act: high growth, strong earnings and a culture of innovation.

These companies are shining a light on the way forward. Illustrating the depth of the challenge, however, was discovering a sizable majority of the respondents came from companies that were lagging behind in their efforts – and paying for it with sluggish revenues and growth, while showing little innovation outside their R&D departments. And yet, sluggish revenues and growth are just harbingers of what might be ahead. When it comes to falling behind in today’s industrial sector, the company that hesitates could well be lost.

There’s a fundamental shift that we’re seeing take place among the sector leaders toward strategic risk management, using risk management as a tool in aggressively and confidently pursuing strategic imperatives. Leaders are looking at the strategic risk universe, as opposed to only focusing on compliance and operations. Even innovation is being considered in terms of risk management.”

William Thomas EY Americas Advisory Risk Sector Leader, Industrial Products

THE URGENCY

In the Transformative Age, you must keep relentlessly moving forward. Proactive disruption has come to the industrial sector. Industry innovation leaders are launching everything from new business models to highly connected ecosystems to smart factories. Thus, every decision to put off launching a digital transformation initiative, for whatever reason, puts that company months behind its traditional competitors — and less able to respond to competition from unexpected sources fueled by innovative applications of emerging technologies.

Since the value chain is being reinvented, your choice is to be a part of the reinvention – or subject to it. The longer you wait to invest in the pieces that enable this reinvention, the more limited your choice is — your chance to lead the disruption, or at least ride the crest of its wave, is reduced; the likelihood of having that wave crash down on you and crush your prospects increases.This urgency is what makes the balancing act so excruciating. At the same time as you need to stay abreast of the innovation happening throughout your sector and respond to more demanding customer expectations, you need to stage the pace of your change so that the rest of your increasingly complex ecosystem stays with you. That’s why, even in our focus on simply planning for the future, we recognize that there is an equilibrium to be maintained.

THE WAY FORWARD

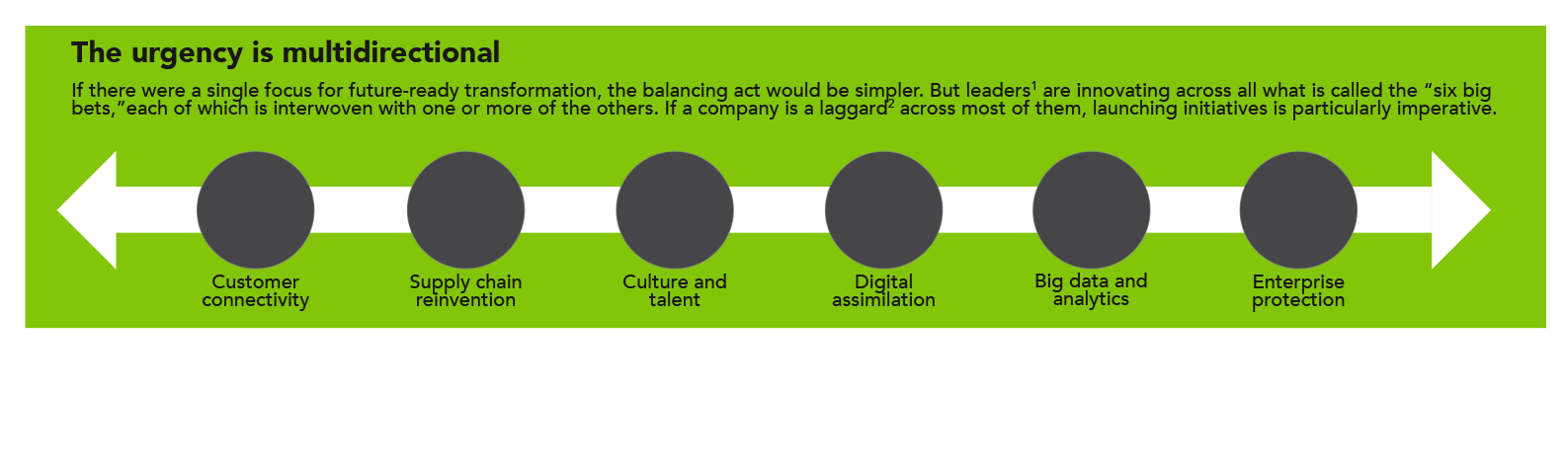

How industry leaders are investing in the big bets. And what you can learn from them.

If there is one overarching theme to the way industrial company leaders are looking at the big bets, it’s that they are making a strategic move from a business-to-business (B2B) framework toward being more business-to-customer (B2C). You can see how this plays out in each of the big bets — and how each of them is interlaced with the others.

Customer connectivity. Customer expectations have changed. They want that same 5 p.m.-to-9 p.m. at-home experience in their 9-to-5 workplace environment. Thus, interactivity, intelligence and awareness have become key aspects of industrial companies’ increasingly customer-centric engagement model. This is why close to half of the executives at companies in the “leader” category in our research are focused on improving their speed and quality. Nearly half also say they are enhancing channels available for customers to order and augmenting their existing products with services to better respond to their customers. This brings digital capabilities into play, to collaborate with business partners.

Such cross-pollination leads to the rapid emergence of new business models — out of necessity: digitally enabled disrupters, often from outside the sector, are forcing industrial companies to think and act differently. This, in turn, puts new stressors on the value chain, which will fragment as industries converge and new the way forward economies emerge. One of those new economies: selling the insights produced by tailored data analytics. The connectivity that makes all this possible, however, also introduces a different risk profile, particularly with increased connectivity with third parties.

Supply chain reinvention. Your supply chain is not just an operational function — it’s a customer experience. This underlying theme represents the biggest difference in supply chains between leaders and laggards in our research: leaders focused their supply chains on improving customer experience. In order to do so, leaders are investing innovation budgets in big data (55%) and driving organizational change (41%).

![]()

Of course, “chain” is no longer the right metaphor: today’s supply chains are no longer linear, but complex ecosystems. They’ve migrated from on-premises to the cloud, which alters the whole notion of collaboration, with suppliers, with other third parties, even with customers. With all data cloud-based, the supply chain is better connected to more intelligence derived from data and, therefore, more responsive; it’s easier to build your ecosystem — and adjust it on-demand. Communications are multidirectional, with information-sharing throughout the entire ecosystem. Digital enablers support the end-to-end process improvement that make enhanced customer responsiveness possible, yet the increase in connectivity also threatens supply chain resilience. These are all considerations along the supply chain reinvention journey.

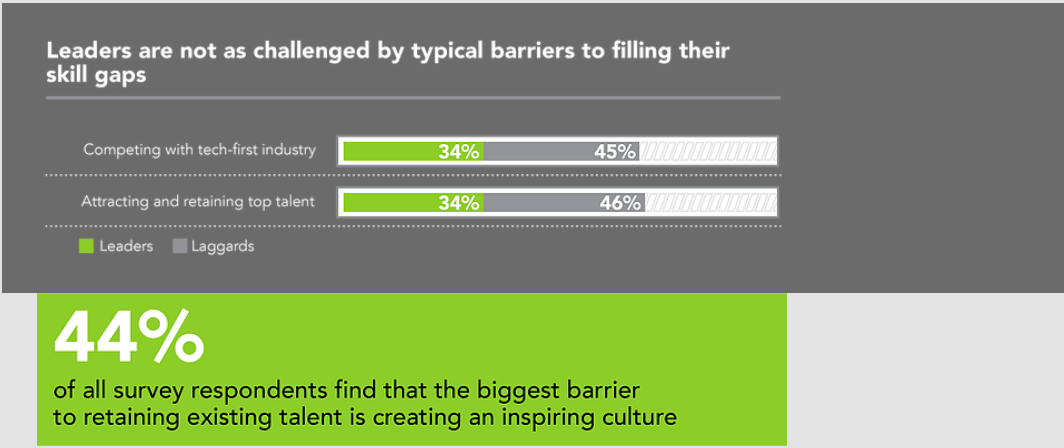

Talent and culture. Industrial companies are thought to be risk-averse and slow to change. That perception played into the difference between leaders and laggards in our research dealing with talent and culture. Leaders aren’t as challenged by typical barriers to filling their skills gaps: competing with tech-first industry (34% for leaders to 45% for laggards) and attracting/retaining top talent (34% to 46%). More differentiating, one of the biggest drivers behind tech investments for leaders is to attract top talent (48% to 23%), while laggards still focus more on operational efficiency (32% for laggards to 14% for leaders).

Industrial companies are playing the culture card by creating a more purposeful work environment to attract the Millennials. That a lot of emerging technologies are targeting the industrial sector is also building appeal — Mmillennials are able to work with cutting-edge tech and apply it in unprecedented ways. This isn’t just about attracting talent. It’s also about keeping them. Across all survey respondents, the biggest barrier to retaining existing talent (44%) was creating a culture that inspired them.

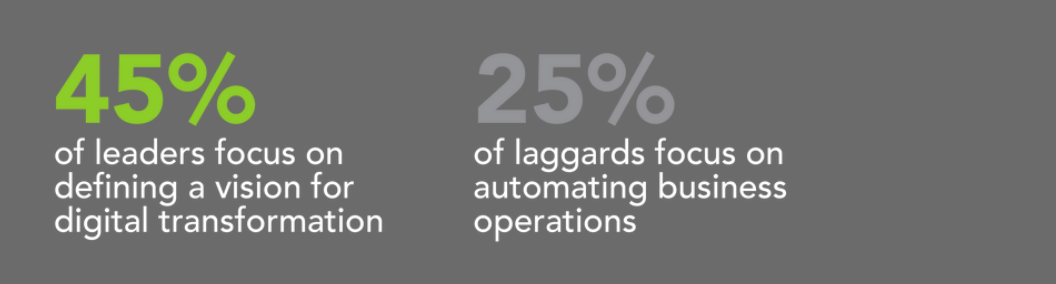

Digital assimilation. The research shows that leaders and laggards think differently about digital as a means for facilitating innovation and growth. While leaders focus on defining a vision for digital transformation (45%), the laggards are more tactically focused on automating business operations (52%). Of course, innovation is not just about creating ideas, but bringing them to market effectively, which is why digital assimilation requires an agile culture.

Digital is an enabler, a means rather than an end. Your strategic process should be to develop the solution first, then infuse it with the necessary technology to bring it to life. You can see this in the smart factory, where digital technology raises productivity by empowering the worker on the shop floor. But ultimately, digital assimilation means evolving from “doing digital” to “being digital” — where digital is deeply ingrained and part of the basic thought process.

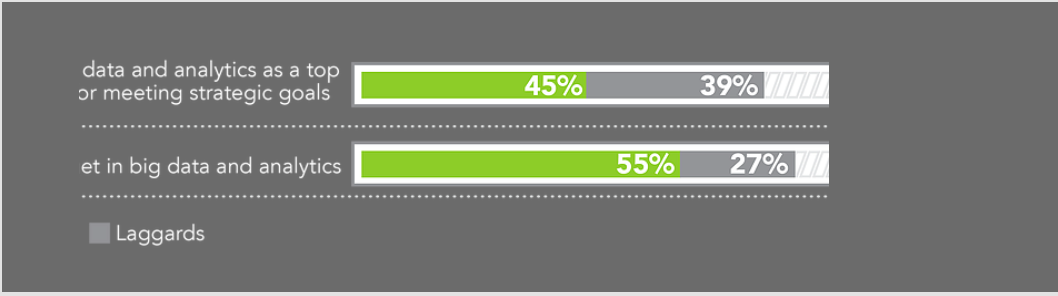

Big data and analytics. Data is the language of innovation. But the challenges of working with today’s data are captured by the four V’s of big data: volume, velocity, veracity and variety. That’s why we call it big data and not simply data. Research reveals a major difference here between leaders and laggards: laggards talk about big data while leaders act on it. There is little difference between leaders and laggards in identifying big data and analytics as a top technology for meeting strategic goals (45% to 39%), but leaders pulled away in devoting a major part of their investment budget to it (55% to 27%). The leaders take advantage of the situation and leverage the technology and available data to differentiate themselves from their competitors.

Data is the new natural resource, but to make productive use of data requires a system that can really manage them. This involves developing a data management platform that will handle gathering the data, curating/integrating them and then activating the data to produce insights (involving data visualization and predictive modeling tools). But data management also requires governance policies to prevent your data lake from becoming a data swamp.

Enterprise protection. Enterprise protection has its own balancing act, between compliance risk, operational risk and strategic risk. When our survey asked about the 10 highest-priority risks, more than half of the risks named didn’t even exist for industrial companies 10 to 15 years ago — digital operating models, robotics, customer focus, 3D printing. At this point, these are all strategic opportunities that require sound risk mUanagement to seize competitive advantage and support successful deployment.

But they also are largely distributed risks as opposed to centralized, top-down risks — decisions on 3D printing should be made in your manufacturing facilities, not in the C-suite. Cyberattacks are more likely to breach security out in the field than at corporate headquarters. Ecosystems need to be able to expand in real-time, in response to newly emergent threats — and opportunities. But every new hand-off presents a new risk. Your risk-management model has to align to this reality — because innovation happens out on the periphery. In this way, risk management is like the brakes on a car: you don’t install brakes just to slow the car down; they’re there to make it safe to go faster.

THE BOTTOM LINE

Find the balance that’s right for you. The balancing act is at least as daunting as the challenges of the Transformative Age itself. No matter where you fall on the laggard-to-leader spectrum, you haven’t completely missed the train. Every company has its own distinctive circumstances and challenges. Every company has its own optimum strategy for moving forward and engaging the digitally enabled future.

But you must rigorously assess your present status and the universe of change options you can entertain. Then, piece together the most “balanced” package of change initiatives to enable you to get the most mileage out of your investments, both in the near-term and beyond.

“Digitization or data assimilation is not an option. It’s a ’must have‘ for every company to remain competitive. Market leaders will be the ones who can embrace the change and bring their innovative ideas to the market faster than their competitors.”

Ranabir Bhakat Executive Director, Enterprise Intelligence Advisory, Ernst & Young LLP